Eduardo Ferreira de Lemos

Energy Practice Lead at Bain & Company

”Distributed generation keeps scaling, but the Winners will think beyond the Asset "

Evolution and drivers of B2B market in Distribute Generation (DG) trends

Distributed Generation (DG) is proofing to be one of the most dynamic and strategic segments in the European energy landscape – especially in the Commercial & Industrial (C&I) segment, where players are rethinking how they source, manage, and optimize energy. With ~65.5 GW(1) of PV installed across the EU in 2024 (up 4% vs. 2023), cumulated installations now exceed 338 GW(2), ~40% of which – roughly 135 GW – is in the C&I segment.

While the pace of growth has slowed compared to past years, the trend remains solid and forward-looking: by 2030, total EU solar capacity is expected to reach ~816 GW(3), of which over 300 GW are estimated to be in the C&I space. This makes DG a long-term, structural opportunity.

Behind-the-Meter (BtM) services and products are emerging as new opportunities within these DG trends. As industry moves downstream, DG offers a way to unlock new value pools by bringing generation closer to demand. The shift is driven not only by regulatory support, but also by deep structural forces: persistent geopolitical risk, macroeconomic uncertainty, and the need for greater energy security are pushing B2B players to take control.

At the same time, high volatility in electricity prices – spiking above €200/MWh for C&I users between 2021 and 2023, and now stabilizing at structurally higher levels vs. 2020 – has increased the appeal of on-site generation as a hedge.

Emerging customer needs and investment priorities

Within this context, C&I demand is evolving fast. Businesses are increasingly integrating on-site assets into their energy sourcing strategy, not just for sustainability reasons, but to stabilize costs and gain autonomy. Four shifts are especially shaping investment priorities today:

- A growing preference toward low-CAPEX models and flexible solutions, such as PPAs;

- Demand for “Energy-as-a-Service” offerings that bundle generation, supply, and optimization;

- Cross-product integration across portfolios (e.g. solar PV, BESS, demand-response);

- A clear expectation of technical depth and delivery reliability from energy solutions providers

The rise of Corporate PPAs confirms this shift: in 2024, 7.6 GW(4) of capacity was contracted in Europe – up 22% vs. the previous year – demonstrating growing appetite for long-term, low-risk energy sourcing models.

However, some structural threats could still hinder the scale-up of DG and challenge the 2030 targets. Grid infrastructure and cross-border interconnectors remain insufficient, increasingly leading to congestion, negative prices and curtailment – with Germany alone curtailing ~9.3 TWh of RES generation in 2024, including ~1.4 TWh from PV(5). Electrification of final demand is progressing slower than needed, while support schemes are being revised or reduced across countries (e.g. transition from net metering to net billing). Permitting bottlenecks also continue to delay deployments.

In light of the growing structural challenges and a market evolving rapidly alongside shifting C&I customer needs, the real competitive edge for DG players lies increasingly in the business model, and not in the hardware. The most successful operators are combining long-term PPAs with integrated Behind-the-Meter (BtM) services and product offerings that act as both enablers of customer value and mitigants against rising challenges. These models embed long-term PPAs, energy management systems (EMS), onsite storage and demand response to dynamically align consumption with generation.

The result of this strategy is recurring value creation, stronger customer stickiness, and improved returns. Turnkey-only players, by contrast, may struggle to scale, as their contribution is limited to short-term margin capture without lasting engagement.

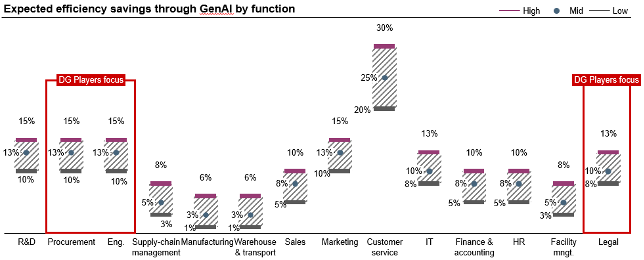

The role of AI in optimizing DG systems

Lastly, the role of AI should not be underestimated. As distributed systems become more complex and data-rich, AI unlocks meaningful efficiency gains – particularly in engineering, procurement, and asset performance optimization, with early adopters reporting cost reductions of 10–15%(6).

To conclude, DG is no longer about solar panels installations, but it is the pillar of a growing BtM profit pool, driven by customers and context priorities and enabled by smart, integrated delivery models. DG players that understand this shift – and act accordingly – stand to lead the next wave of value creation.

Know more about our DG Solutions and trends with Greenvolt Next

Latest News